One of the side effects of the pandemic is the explosion in the savings rate and the level of deposits at financial institutions. Many institutions have lowered their deposit rates because with loan demand down and investment yields at historical lows they want to encourage people to take their money elsewhere. Is this really the best thing to do?

When the cost of funds is determined by interest rate alone, even at 0.01% checking accounts can look expensive when compared to available investment yields. However, a better way to look at deposits is from a Net Cost of Funds perspective. This concept provides a broader picture of the true value of deposits.

Net Cost of Funds recognizes there are costs associated with deposits beyond interest expense. This includes processing costs for debit cards, ATMs, checks as well as employee costs of contact centers and branches. As important, there is income to be made from

transaction accounts in the form of interchange and NSF/Courtesy pay among other things. Sure, for non-transaction accounts it is more about the rate of interest than net operating costs, but for transaction accounts net expense, which includes non-interest income, is important.

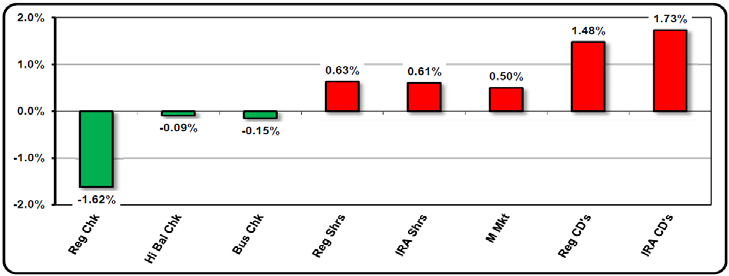

In many cases, Net Cost of Funds is negative for accounts where non-interest income is greater than non-interest expense plus interest expense as shown below.

Average Credit Union Net Cost of Funds %

In fact, as the graphs show, most Kohl clients make money outright on their transaction accounts. Therefore, even if there is no loan demand and investment yields are low, if your Net Cost of Funds is negative, your institution can make money on these transaction accounts even if you just put cash in the vault.

Average Net Cost of Funds %